Buying a Home with Low or No Down Payment: What You Need to Know

Buying a Home with Low or No Down Payment: What You Need to Know

Many people believe they need a 20% down payment to buy a house, but it’s possible to purchase a brand-new house with as little as 3.5% down — or nothing down at all. While a larger down payment is helpful in many situations, several factors determine how much money you’ll actually need for the home purchase.

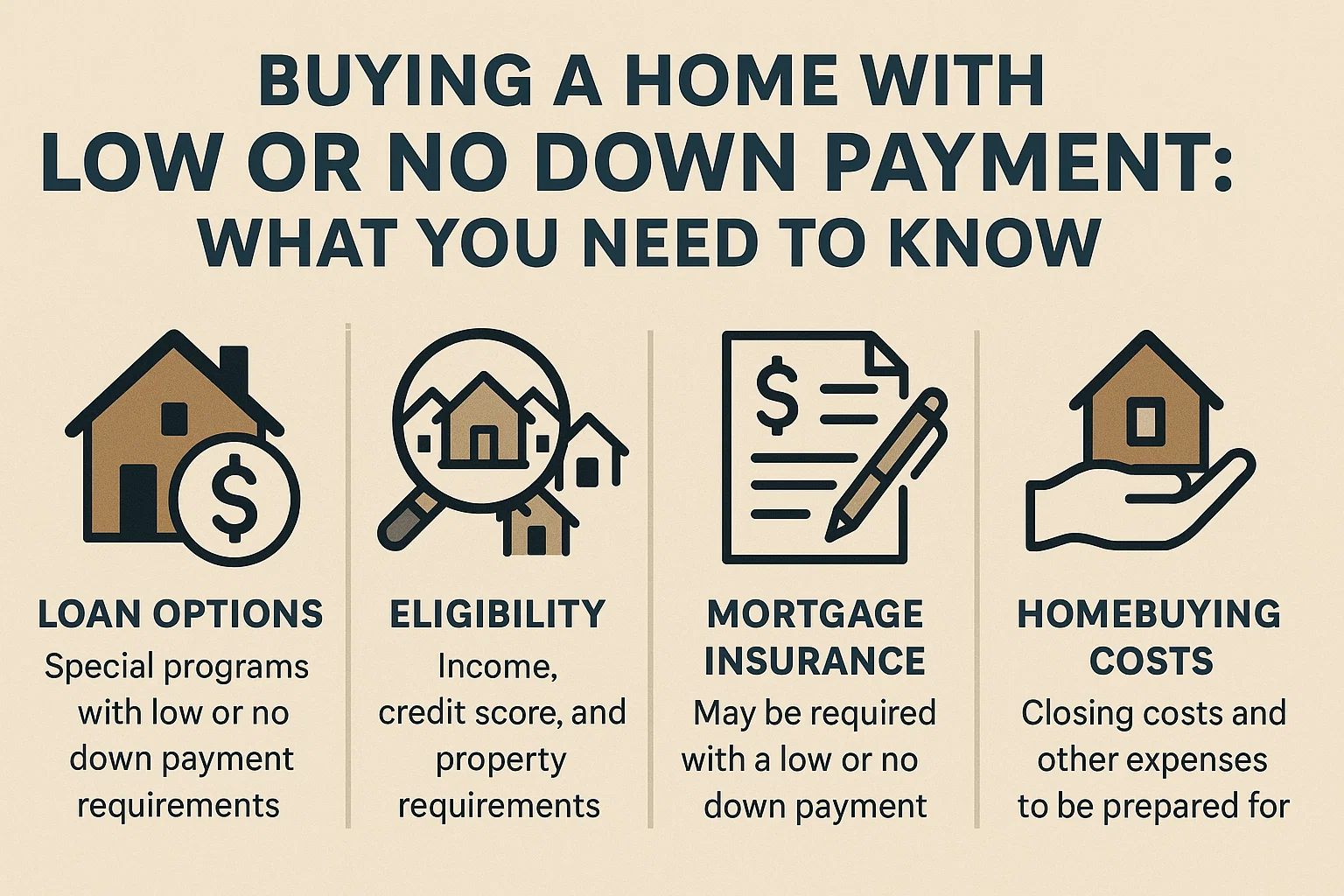

How Much Money Do You Need to Buy a House?

In addition to the down payment, there are other expenses beyond the listing price of a home. Most of these fall under closing costs, which include:

- Earnest deposit

- Property inspection and appraisal

- Title insurance

- Portion of property taxes

It’s estimated you’ll need between $7,000 and $10,000 set aside for closing costs, in addition to your down payment.

What Is a Down Payment?

A down payment is an up-front payment toward the total cost of the home, expressed as a percentage of the purchase price. Lenders often require a minimum down payment to approve a home loan.

What Can That Down Payment Look Like?

Conventional Loans

- Minimum 5% down for loans up to $417,000.

- Minimum 10% down for loans above $417,000.

- Programs like Fannie Mae’s 3% down option are also available.

FHA Loans

- Minimum 3.5% down (e.g., $8,750 on a $250,000 home).

- Backed by the Federal Housing Administration (FHA).

VA and USDA Loans

- 0% down required for eligible buyers.

- VA loans: Available to active-duty military personnel, veterans, and qualifying groups.

- USDA loans: Available in rural and suburban areas.

Note: Down payments can often include gifts from family or funds from assistance programs.

Mortgage Insurance

Low-down-payment loans typically require mortgage insurance or a funding fee:

- FHA loans: Always include mortgage insurance.

- VA loans: Include a one-time funding fee.

- 20% down usually waives mortgage insurance for conventional loans.

Exceptions for New Construction

Custom-Built Homes

Lenders may require a larger down payment (via construction-to-permanent loans) since the home doesn’t yet exist.

Condos and Townhomes

Requirements vary based on lender guidelines, loan type, location, and pre-sale status. Confirm eligibility with your lender.

Get Prequalified

Most buyers don’t need a large down payment—or any at all. To explore your options, talk to a lender about prequalification and loan programs.