Are You Self-Sidelining Your Dream of Homeownership? Debunking Common Mortgage Myths

Are You Self-Sidelining Your Dream of Homeownership? Debunking Common Mortgage Myths

Are you not considering buying a new house because you don’t think you’ll qualify for a home loan? Don’t have enough money saved up for a down payment? Think your credit score isn’t high enough? If so, you are one of perhaps millions of mistaken wannabe homeowners who, for these reasons or others, decide for themselves that they aren’t financially ready to purchase a home before they even try to find out if they are.

“Consumers are more cautious than they have been in the past” and are “self-sidelining” themselves, according to Archana Pradhan, an economist at CoreLogic, a real estate information company. There’s no telling how many people are taking themselves out of the game without even trying. But, according to CoreLogic’s numbers, loan applications last year were half what they were in 2005 when the housing market was booming. At the same time, the denial rate has fallen by roughly one-third.

This tells Pradhan – and others – that folks haven’t even tried to obtain a mortgage like they did in the years prior to the Great Recession, largely because they don’t think they can make the cut. After all, if credit underwriting standards have tightened, as has been widely reported, then how else could it be that fewer applicants are being rejected? “The observed decline in originations could be the result of potential applicants being too cautious,” says the CoreLogic economist.

Student Debt

This is a real issue, no doubt about it. According to some sources, grads with a four-year degree leave college with $35,000 in debt. Those who go on to grad school owe $53,000 to $54,000. That’s the bad news. The good news? Some lenders will roll student debt into the mortgage amount, lessening the load with today’s near-record-low mortgage rates—often half the rate of student loans.

Credit Score

The average borrower credit score has increased from 700 in 2005 to nearly 750 in 2015, per CoreLogic. However, lending to “subprime” borrowers with scores below 620 has also risen. “Lending is matching the market very well,” says Sam Khater, CoreLogic’s deputy chief economist. In 2015, loans to borrowers with scores ≤620 increased by nearly 25% over 2014, a trend continuing into 2025, according to Equifax’s Amy Crews Cutts.

While conventional lenders often favor higher scores, FHA-backed loans accept scores as low as 580. EllieMae reports 27% of loans closed in May had scores below 600, some even below 550. If your score needs improvement, address credit report errors, adjust credit habits, or take federally approved credit counseling courses. Better scores can lower costs for insurance, cell phones, and rent, too.

Down Payment

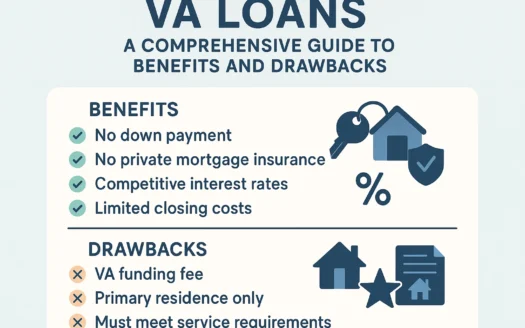

Many believe they need 20% down, but FHA loans require just 3.5%, and VA loans for veterans require $0 down. EllieMae data shows the average FHA down payment is 4%, while VA down payments average 2%.

Fear

Some fear rejection or interacting with loan officers, assuming they’re pushy salespeople. Not true—loan officers must pass licensing exams and complete continuing education. Approvals are handled by underwriters you’ll never meet, preventing pressure to accept unsuitable loans. A reputable loan officer can explain products, terms, and options tailored to your needs.

TD Bank’s survey of 1,300 homebuyers found one-third had an “excellent” lender experience, while 75% rated their experience “very good” or “excellent.”

Cumbersome Process

Many, especially Millennials, avoid homebuying due to perceived complexity or face-to-face interactions. However, most lenders offer online platforms to research and apply for loans at your own pace. Paul Anastos, president of Mortgage Master, notes the myth that Millennials only want digital interaction but emphasizes lenders offer flexible communication until buyers are ready to engage personally.

Builders also provide digital tools to explore floor plans, options, and communities online. While in-person visits are eventually necessary, initial research is just a click away.