A Comprehensive Guide to Mortgage Points: Savings, Calculations, and Key Considerations

A Comprehensive Guide to Mortgage Points: Savings, Calculations, and Key Considerations

Understanding Mortgage Points

A new home is often the most expensive purchase you’ll ever make. Beyond the price of the home itself, costs accumulate throughout the buying journey—from researching locations to negotiating loan terms. Mortgage points offer a way to reduce long-term expenses by lowering your mortgage interest rate, potentially saving thousands over the life of your loan.

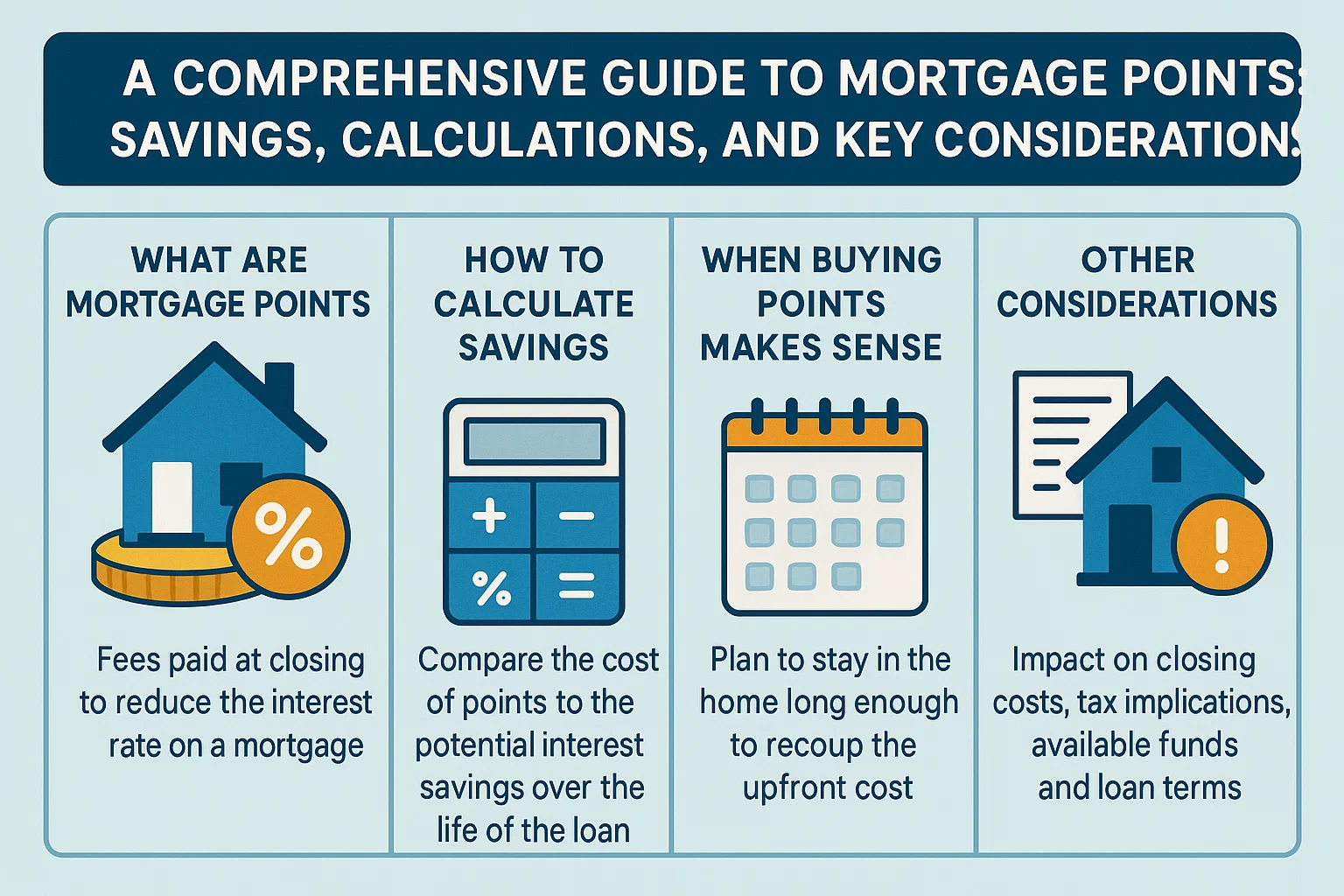

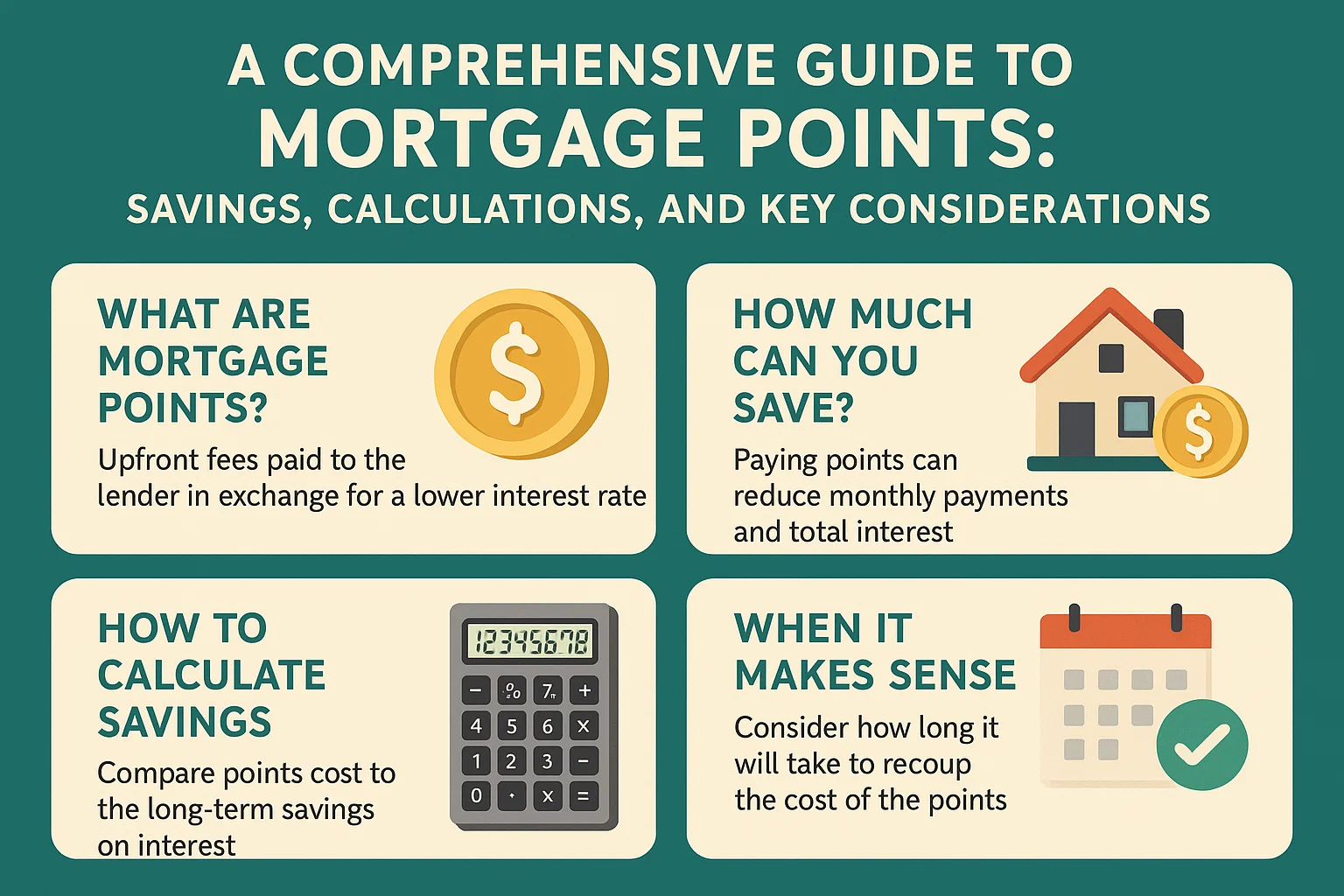

What Are Mortgage Points?

Mortgage points (or discount points) are upfront fees paid at closing to reduce your mortgage interest rate. Each point typically lowers your rate by 0.25%, though this varies by lender. While points don’t affect your loan principal, they decrease the total interest paid over time. This strategy is ideal for long-term homeowners, as savings compound over years.

How Mortgage Points Work

Two Types of Mortgage Points

- Origination Points: Fees charged by lenders for processing your loan. These are part of closing costs and do not lower your interest rate.

- Discount Points: Prepaid interest to reduce your mortgage rate. The more points purchased, the greater the rate reduction.

Cost of Mortgage Points

Each discount point costs 1% of your loan amount. For example:

- A $200,000 loan would cost $2,000 per point.

- Points can often be purchased in increments as small as 0.125%.

Calculating Savings with Mortgage Points

Example: A $200,000 30-year fixed-rate mortgage at 5.125% costs $392,028.20 over 30 years. By purchasing 1.75 points ($3,500 upfront), the rate drops to 4.75%, reducing total interest to $375,480. This saves $16,549.20 over the loan term, or about $45.97 monthly.

The Break-Even Point: Why It Matters

The break-even point is when savings from reduced interest equal the upfront cost of points. To calculate:

- Divide the total cost of points by monthly savings:

$3,500 / $45.97 = 76.14 months (≈6.34 years).

If you plan to sell or refinance before this point, mortgage points may not be cost-effective.

Benefits of Mortgage Points

- Lower interest rates and monthly payments.

- Long-term savings on interest.

Key Considerations

- Higher upfront closing costs.

- Opportunity cost (e.g., paying off other debt).

- Your financial stability and homeownership timeline.

Mortgage Points FAQs

How many points can I buy?

Most lenders allow 0–3 points.

Are points tax-deductible?

Discount points are deductible; origination points are not.

Do points reduce the principal?

No—they only lower the interest rate.

Can points be used with adjustable-rate mortgages (ARMs)?

Yes, but savings apply only to the fixed-rate period.