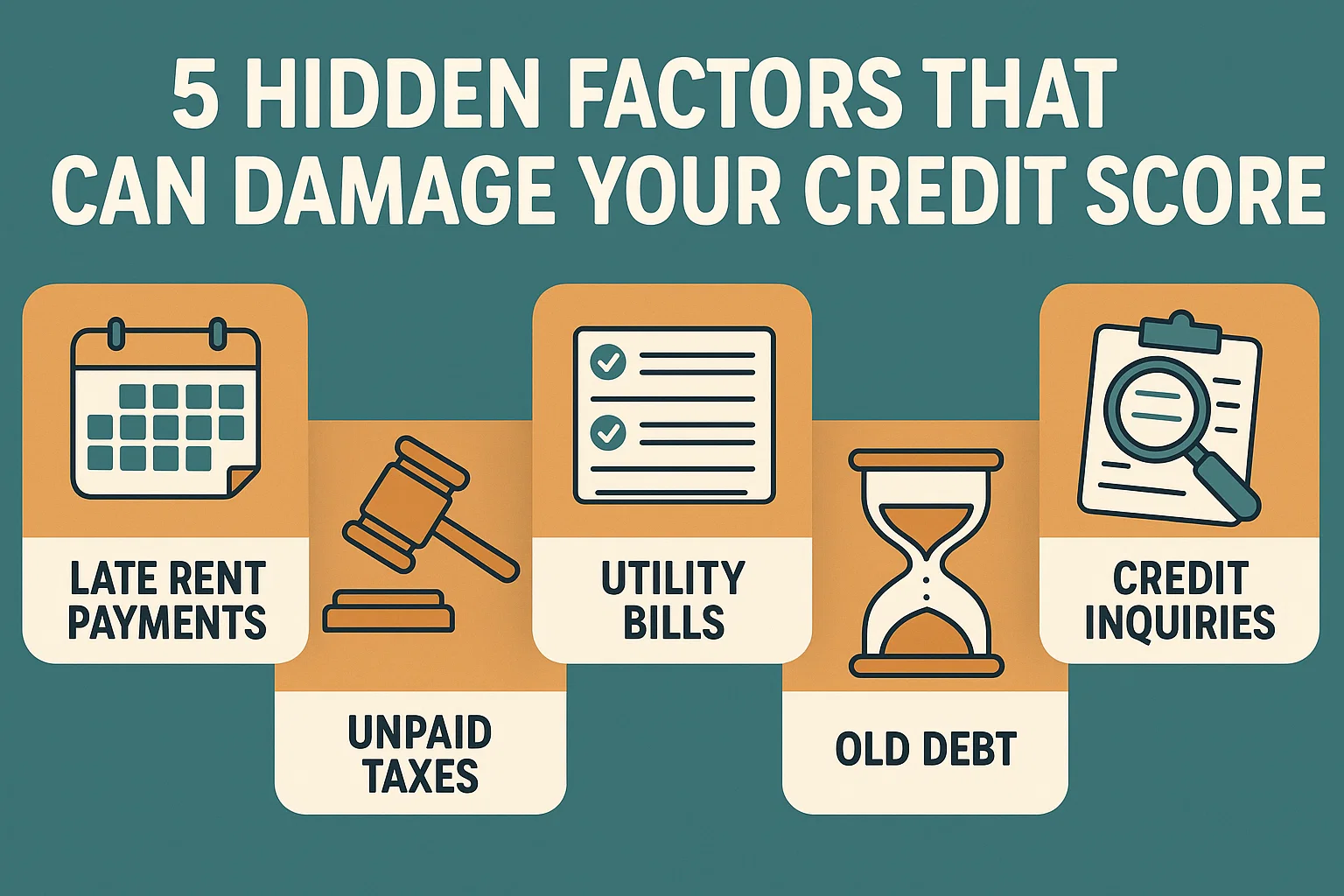

5 Hidden Factors That Can Damage Your Credit Score

5 Hidden Factors That Can Damage Your Credit Score

Your credit score is influenced by more than just loans and credit card payments. Everyday financial habits and overlooked obligations can quietly undermine your financial health. Here’s what you need to watch out for:

1. Overdue Accounts Sent to Collections

Unpaid bills for utilities, medical services, parking tickets, gym memberships, or even library fees can be transferred to third-party debt collectors. These agencies often report delinquent accounts to credit bureaus, which then appear on your credit report and lower your score.

2. Unresolved Tax Liabilities

While late tax payments don’t immediately hurt your credit score, prolonged non-payment can trigger serious consequences. The IRS may file a Notice of Federal Tax Lien against you, which becomes a negative mark on your credit report and significantly reduces your score.

3. Frequent Credit Card Applications

Every time you apply for a retail store credit card or loan, lenders perform a hard credit inquiry to review your financial history. These inquiries remain on your credit report for two years and temporarily lower your score—even if your application is denied. Multiple inquiries compound the damage.

4. Closing Unused Credit Cards

Closing a credit card—even with a $0 balance—can harm your score in two ways:

- Reduces your total available credit, which may increase your credit utilization ratio (the percentage of credit you use relative to your limit).

- Shortens the average age of your credit history, a factor in calculating your score.

5. High Credit Card Balances

Regularly using more than 30% of your credit limit can lower your score. For example, a $10,000 limit means keeping balances below $3,000. Maxing out cards signals financial strain and poses a higher risk to lenders.

Key Definitions

- Hard Credit Inquiry: Occurs when a lender checks your credit report during a loan or credit card application. Multiple inquiries suggest higher borrowing risk.

- Credit Utilization Ratio: Calculated by dividing your total credit card balances by their combined limits. Aim to keep this below 30%.