Understanding FHA Loans: Key Benefits and Considerations for Homebuyers

Understanding FHA Loans: Key Benefits and Considerations for Homebuyers

For many aspiring homeowners, securing a mortgage can feel overwhelming—especially for first-time buyers or those with less-than-perfect credit. FHA loans offer a government-backed path to homeownership with unique advantages and requirements. Below, we break down how these loans work and what you need to know before applying.

What Is an FHA Loan?

Established in 1934, the Federal Housing Administration (FHA) was designed to make homeownership accessible during economic hardship. Today, FHA loans remain a popular choice for buyers who may not qualify for conventional mortgages. These loans are insured by the FHA and provided through approved lenders, allowing for lower down payments and more flexible credit requirements.

How Do FHA Loans Differ from Conventional Mortgages?

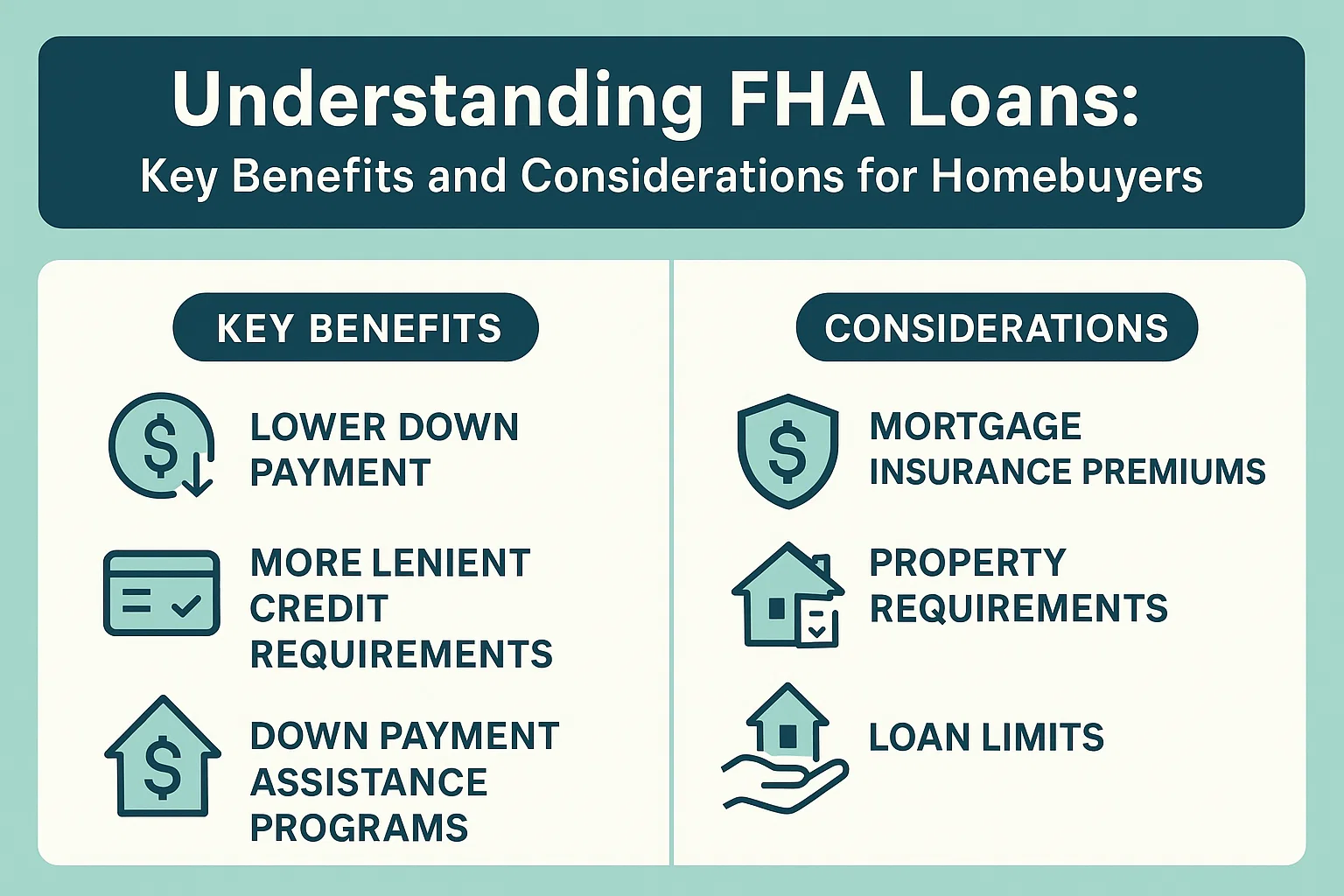

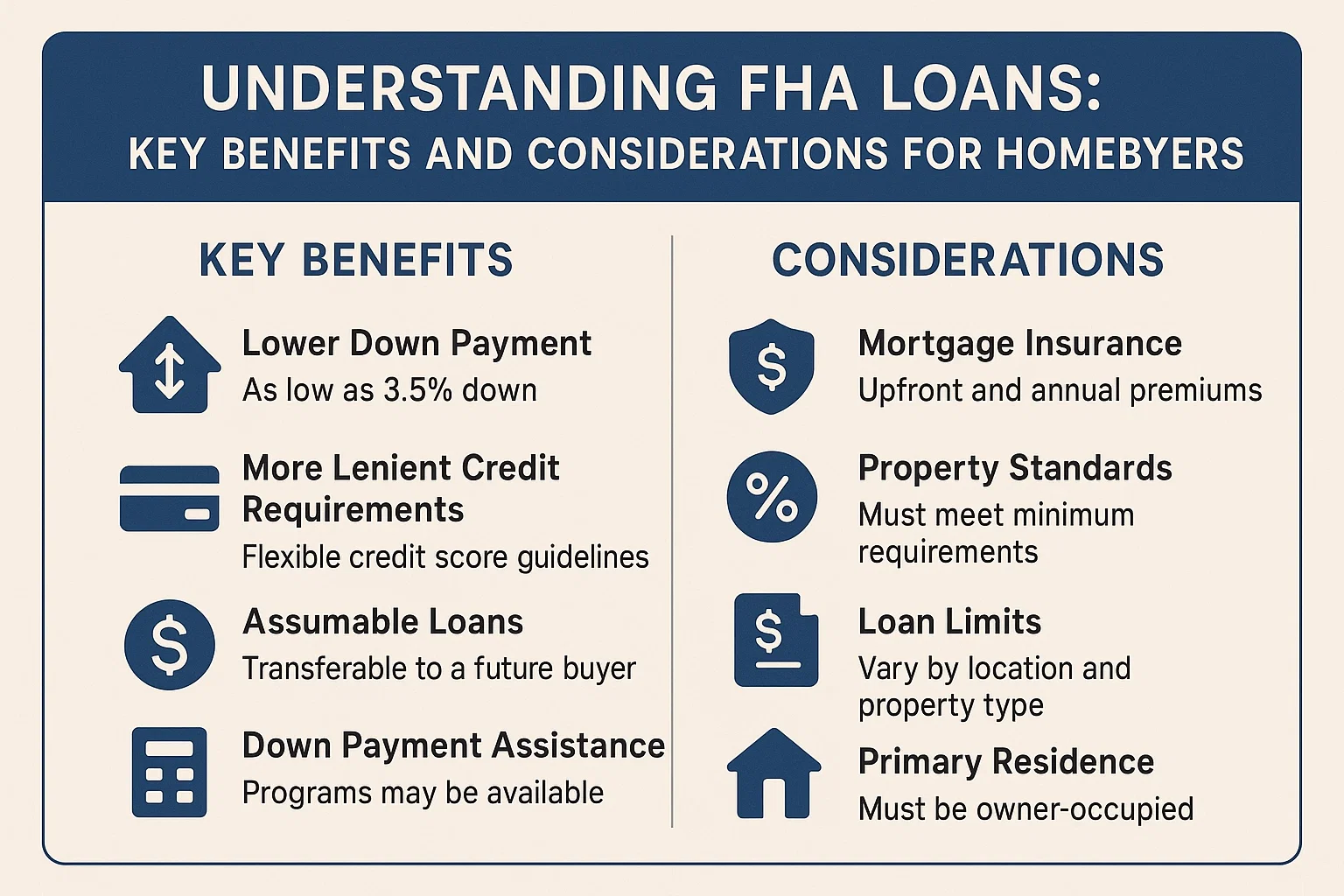

Unlike conventional loans, FHA loans are backed by the U.S. government, which reduces risk for lenders. This enables:

- Lower credit score thresholds (as low as 500 with a 10% down payment or 580 for 3.5% down).

- Higher debt-to-income ratio allowances.

- Access to down payment assistance programs.

However, borrowers must pay mortgage insurance premiums (MIP) for the life of the loan in most cases.

Pros and Cons of FHA Loans

Advantages

- Low Down Payment: As little as 3.5% down with a credit score of 580+.

- Flexible Approval: Easier qualification for borrowers with limited credit history or past financial challenges.

- Refinancing Options: Can be refinanced into FHA or conventional loans later.

Drawbacks

- Mandatory Mortgage Insurance:

- 1.75% upfront MIP fee at closing (can be rolled into the loan).

- Annual MIP payments for the entire loan term unless refinanced or if a 10% down payment is made (then MIP ends after 11 years).

- Property Requirements: Homes must meet strict safety standards and be owner-occupied.

- Loan Limits: Maximum loan amounts vary by location and may restrict higher-priced homes.

How to Apply for an FHA Loan

Follow these steps to begin the process:

- Find an FHA-Approved Lender: Use official resources to locate qualified lenders.

- Gather Documentation: Prepare proof of income, employment history, tax returns, and credit reports.

- Get Pre-Approved: This strengthens your offer when house hunting.

- Home Appraisal: The property must pass an FHA appraisal to ensure it meets livability standards.

Is an FHA Loan Right for You?

FHA loans are ideal for buyers prioritizing lower upfront costs and flexible credit terms. However, the long-term costs of mortgage insurance and property restrictions should be carefully weighed. Consulting a financial advisor or lender can help clarify whether this option aligns with your homeownership goals.

Ready to explore your options? Connect with a reputable financing team to discuss FHA loans and begin your journey toward finding the perfect home.