Cash-Out Refinancing: A Guide for Homeowners Needing Funds

Cash-Out Refinancing: A Guide for Homeowners Needing Funds

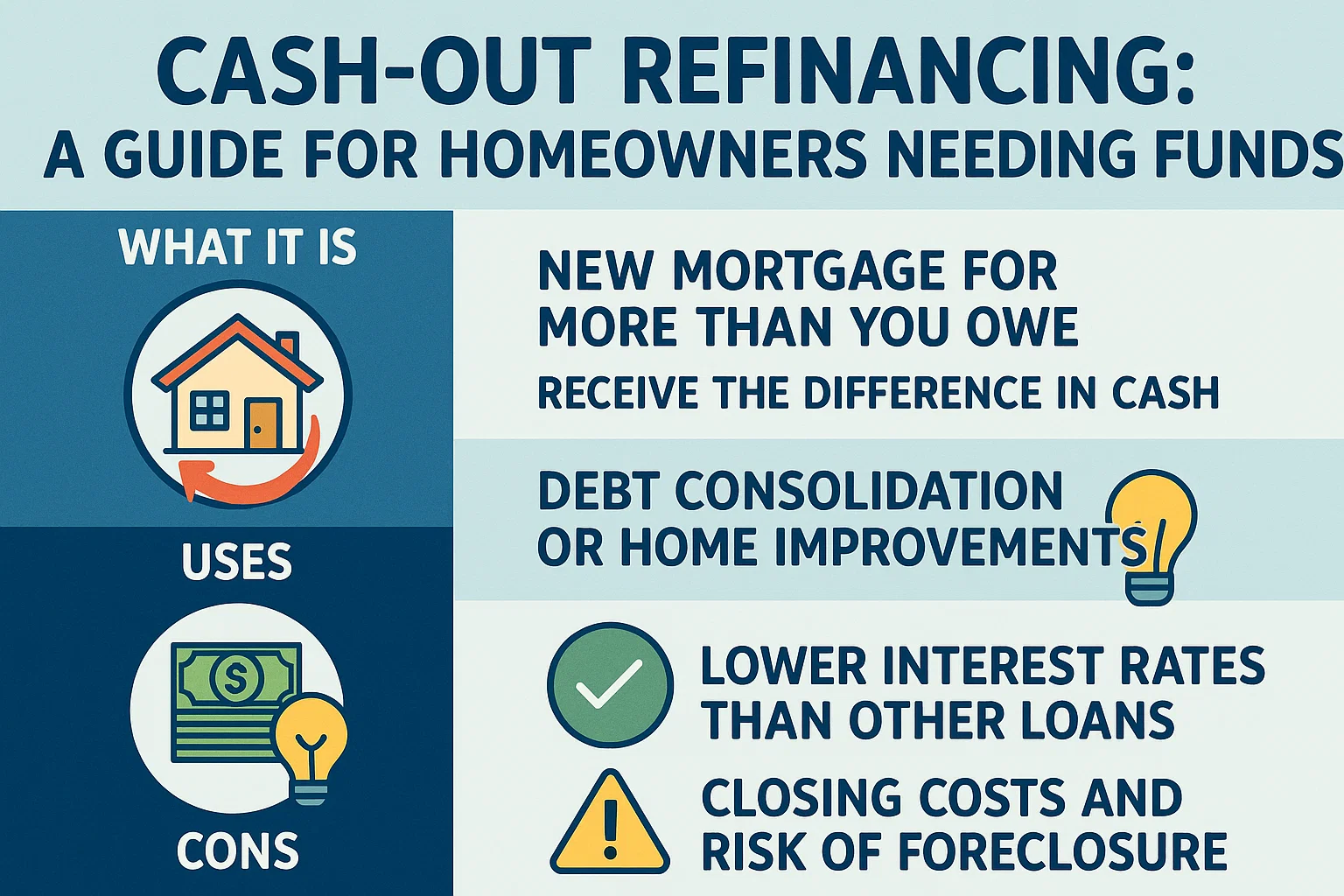

If you’re a cash-strapped homeowner with a solid chunk of home equity in your name, cash-out refinancing is an option worth considering if you need a lump sum of money. In a nutshell, a cash-out refi is a type of mortgage refinancing that replaces your existing mortgage with a new higher amount. You’ll pay off your existing mortgage under the new loan’s terms, and you’ll get a chunk of change to consolidate debts, pay for a major home renovation, or cover any other major expenses. In turn, however, you’ll have a new mortgage, interest rate, and monthly payment to deal with.

Cash-out refinancing isn’t for everyone, and it’s just one of many ways homeowners can leverage their home equity to access funds when they need it. If you’re considering a cash-out refinancing, here’s everything you need to know about how they work and how to apply for one.

What is Cash-Out Refinancing?

Essentially, a cash-out refinance replaces your existing mortgage with a brand new one that comes with a new loan amount, interest rate, terms, and monthly payment. The cash-out refi will be larger than the balance on your existing mortgage, giving you enough funds to pay it off and provide you with an extra lump sum of cash. In short, you’re turning a portion of the home equity you’ve established over the years into a cash payout.

Typically, lenders allow homeowners to borrow up to 80 percent of their home’s market value. Say, for example, your home is appraised at $200,000 and you still owe $100,000 on your current mortgage. You may be approved for a cash-out refinance of $160,000. You’ll use the first $100,000 to clear your current mortgage, leaving you with $60,000 in your bank account.

How Does Cash-Out Refinancing Work?

For starters, you’ll need to find a lender that provides cash-out refinancing, and they don’t necessarily have to be the same lender as the one that issued your initial mortgage. The lender will assess your current mortgage’s terms, your home’s appraised value, how much equity you’ve established, and how much you owe. But they’ll also take stock of factors like your credit score, monthly income, and debt-to-income ratio to see if you can manage a new mortgage and, potentially, higher monthly payments.

From there, they’ll set up a new loan with new terms you’ll be locked in for – one that’s enough to pay off your initial mortgage and provide you with the cash you need. Once your existing mortgage balance is cleared, the rest is paid to you in a lump sum.

As a general rule of thumb, lenders will require that you maintain at least 20 percent of the equity in your home, but this will vary from lender to lender and your initial loan type. If your original mortgage was a Veterans Affairs home loan, for example, you may be eligible to use 100 percent of your home equity under the VA cash-out refinancing program.

What Can I Use a Cash-Out Refi For?

You can use the funds from a cash-out refi on virtually anything you want. But for practical purposes, the wisest ways to use a cash-out refi include:

- To pay for home improvement projects. Most homeowners tap into the home equity to pay for a kitchen renovation, replacing the roof or HVAC system, or constructing an extension to the property. This way, their cash-out refi is helping to build more property value. Bonus: If you’re using your cash-out refi income on “capital home improvement” projects, your mortgage interest is tax-deductible!

- To secure a lower interest rate. Some homeowners opt for a cash-out refi simply to re-establish a new home loan, to either secure a lower interest rate or select longer terms. In both cases, this could lead to lower monthly payments. If interest rates have dropped or your financial situation has improved (higher credit score, more income, fewer debts), you could be in a prime position to score a lower interest rate.

- To consolidate debts. If you’re grappling with credit card debt or payday loans with interest rates of 19.99% up to 46.96%, you may decide to apply for a cash-out refi to wipe these debts clean. Your new mortgage’s interest rate won’t be nearly as high.

- To pay for emergency expenses. Sometimes home equity can be a saving grace if you need to tap into it to pay for unforeseen costs like medical expenses, car repairs, or unemployment.

Ultimately, you’re trading away your hard-earned home equity, so you shouldn’t waste the proceeds of your cash-out refi on frivolous spending.

How Much Will a Cash-Out Refi Cost Me?

Cashing out a portion of your home equity comes at a price: Expect to pay between 2% and 5% of your new loan amount on closing costs. The amount is deducted directly from the “cash-out” you’ll receive. It includes everything from loan origination fees, appraisals, inspections, credit report checks, title examinations, and administrative work.

How much you end up paying in closing costs may be the dealbreaker that stops you from proceeding. If, for example, you only need $10,000 but your closing costs total half of that or more, it may not be worthwhile. Comparison shop between lenders—some offer “no-cost refinancing,” which rolls closing costs into the total loan balance or offers a higher interest rate instead.

What is the Interest Rate on a Cash-Out Refi?

Cash-out refinancing is available with a fixed- or variable-rate mortgage. A fixed rate locks in your rate for the entire loan term, ideal for budgeting. A variable rate could start lower but fluctuate monthly, depending on market conditions.

What Are the Disadvantages of a Cash-Out Refinance?

- You’re taking out a larger loan against your home. This could extend your mortgage term or strain your budget with higher payments.

- You’re borrowing at a premium. Closing costs and potential private mortgage insurance (PMI) if equity dips below 20% add to expenses.

- Your home is collateral. Defaulting on the loan risks foreclosure.

- Potential for overspending. Using equity for non-essential expenses can be financially reckless.

- Slow processing. Approval can take up to two months, making it unsuitable for urgent needs.

How Do I Qualify for Cash-Out Refinancing?

To get approved, you’ll typically need:

- A credit score of at least 600–640 (some lenders accept 580 with strong income/debt ratios).

- A debt-to-income ratio below 50%.

- At least 20% home equity (varies by lender and loan type).

- Homeownership for six months (12 months for FHA loans).

- A successful appraisal, credit check, and underwriting process.