Why a Mortgage Preapproval Letter Outshines Prequalification

When It Comes to Landing a Home Loan, a Preapproval Letter Is Far Better Than a Prequalified Letter. Here’s Why.

As a home shopper, understanding the difference between prequalified and preapproved is critical. Here’s why a preapproval letter holds far more weight:

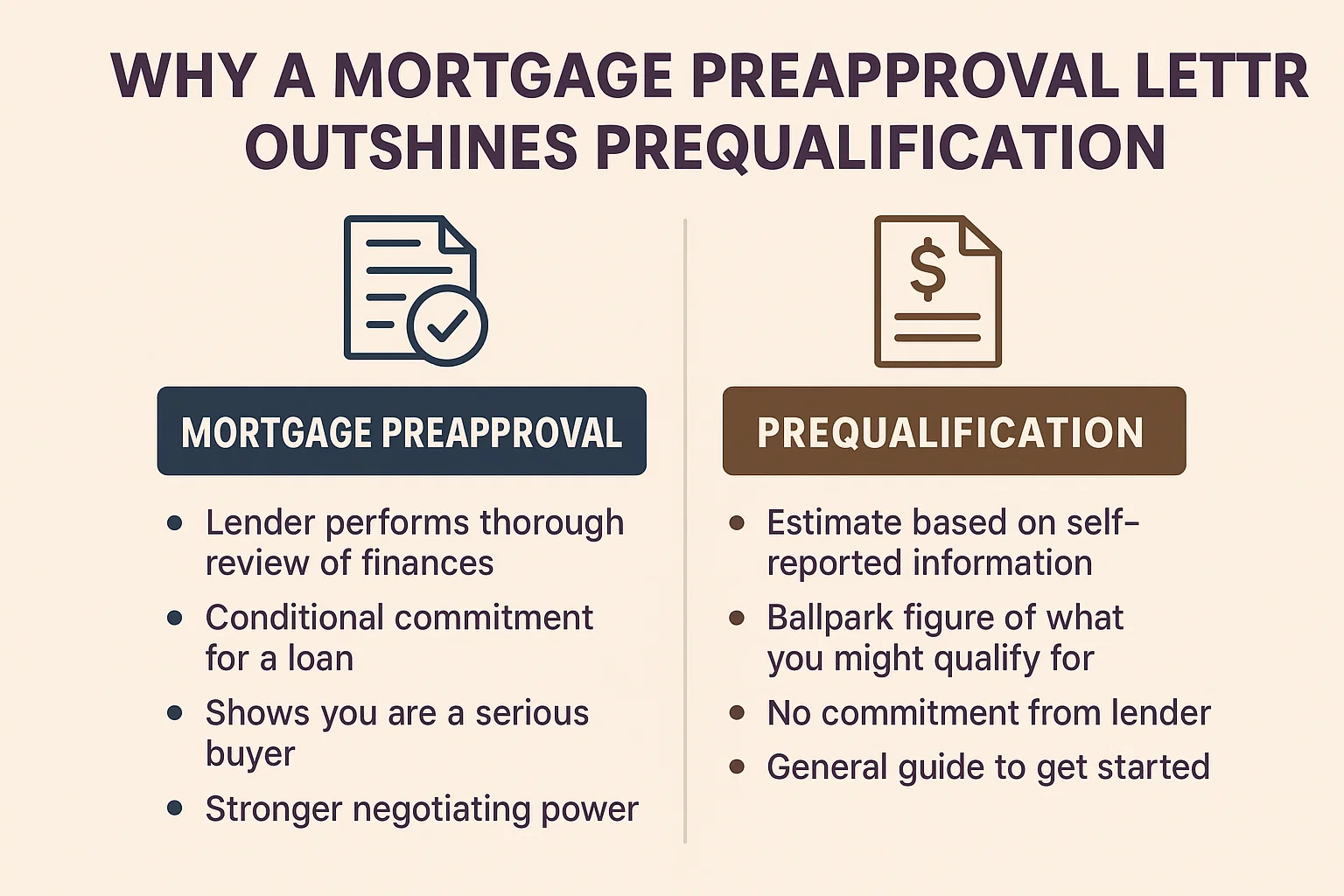

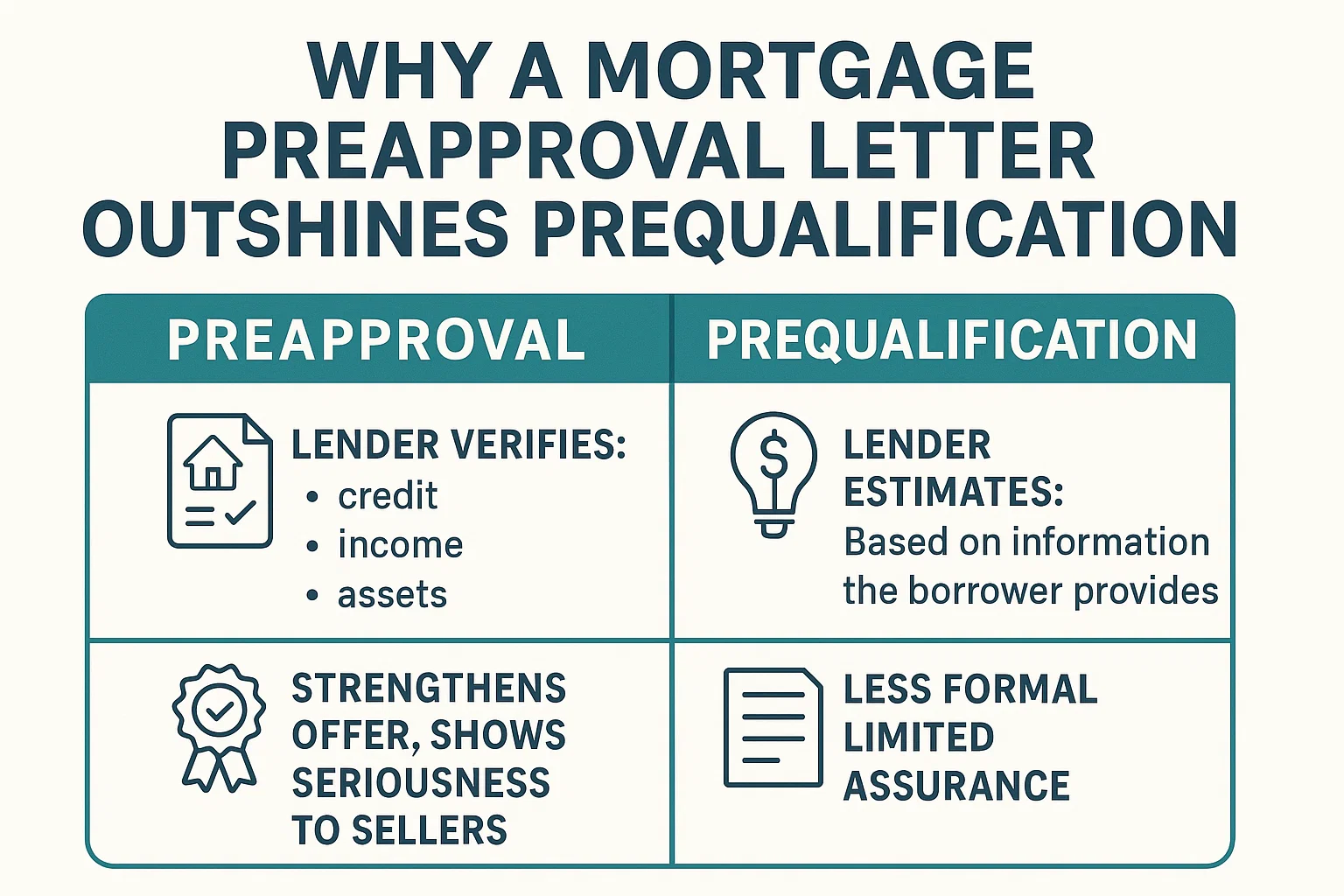

The Problem with Prequalification

A prequalification is often called a “Swiss cheese” loan commitment in the industry. It’s based solely on unverified information you provide, leaving lenders ample room to backtrack. This makes it meaningless in competitive housing markets.

Why Preapproval Matters

A preapproval letter signifies the lender has rigorously verified your:

- Income

- Debt-to-income ratio

- Credit history

- Assets and liabilities

It acts as a written promise (pending appraisal and final checks) that you’ll secure financing for a home within specified terms. This:

- Narrows your home search to properties you can truly afford

- Strengthens your offer against competing buyers

- Demonstrates serious intent to sellers

The Caveats

Even preapproval isn’t bulletproof. Deal-breakers can include:

- Low property appraisals

- Last-minute credit changes (e.g., new debt)

- Title issues

How to Get Preapproved

Expect thorough documentation under current federal lending rules. Required materials typically include:

- Social Security numbers for all applicants

- 2 years of W-2s/tax returns (1099s for contractors)

- 2 months of bank/investment statements

- Details of all real estate holdings and debts

- Credit report payment and appraisal fee

- Explanations for any credit issues

Pro tip: Mortgage preapprovals typically expire in 90 days. Once approved, start house hunting immediately. For lender-specific requirements, review resources like Prospect Mortgage’s preapproval process.

Final Advice

While the paperwork is intensive, a preapproval letter gives you negotiating power and financial clarity. Complete the process early, then focus on finding your dream home within budget.