Timing Your Home Closing: How Month-End Dates Impact Costs and Cash Flow

Timing Your Home Closing: How Month-End Dates Impact Costs and Cash Flow

Why Most Buyers Close Late: Minimizing Upfront Interest

First-time homebuyers often aim to schedule their closings near the end of the month to maximize their final rent checks. However, nearly all buyers—not just newcomers—prefer late-month settlements for another critical reason: reducing upfront interest payments.

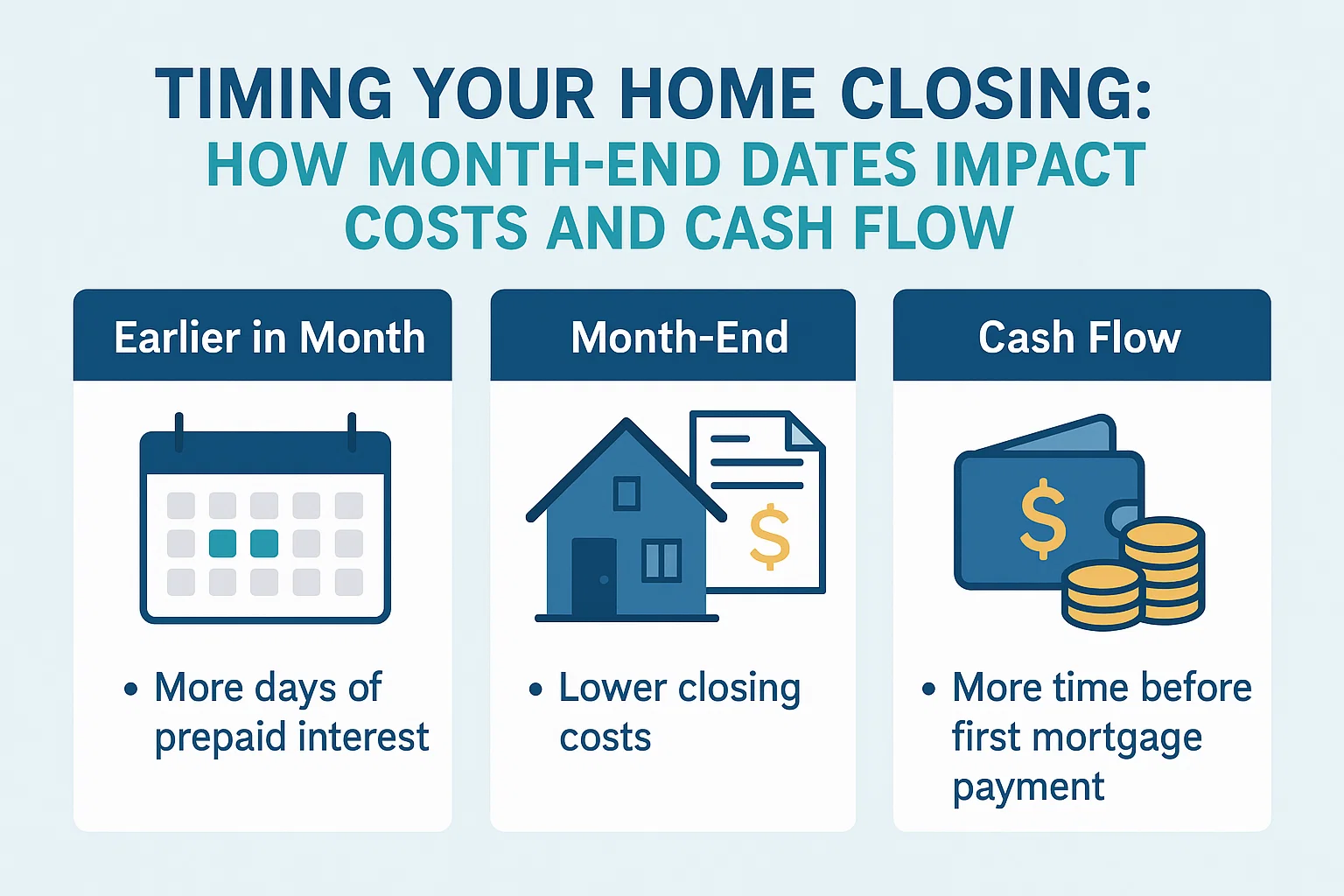

Mortgage interest is collected in arrears, meaning borrowers pay interest for the days between their closing date and the end of that month. For example, closing on May 30 would require paying interest for just two days (May 30–31), whereas closing on May 15 would mean covering 16 days of interest. This difference can save hundreds of dollars in upfront cash, a key consideration for budget-conscious buyers.

Industry data suggests that over 95% of real estate transactions occur in the final week of the month, with many closing on the last business day. This trend reflects buyers’ efforts to minimize immediate out-of-pocket expenses before their first full mortgage payment comes due.

Early Closings: Prioritizing Convenience and Accuracy

While late closings save money, settling earlier in the month offers logistical advantages. Closing agents, lenders, and service providers (e.g., appraisers, insurers) face fewer time pressures mid-month, reducing the risk of errors or delays. As one real estate professional notes:

“Everyone’s scrambling at the month’s end. Mid-month closings often mean smoother transactions and better attention to detail.”

Common mid-month benefits include:

- Fewer scheduling conflicts with inspectors or title companies

- More time to resolve last-minute paperwork issues

- Reduced wait times at busy title offices

Cash Flow vs. Payment Timing: A Critical Balance

Closing later minimizes upfront costs but accelerates your first mortgage payment. For instance:

- January 28 closing: Pay 3 days of prepaid interest. First full payment due March 1.

- January 15 closing: Pay 16 days of prepaid interest. First full payment also due March 1.

While total interest paid remains the same, the timing impacts short-term cash flow. Buyers with limited savings may prefer postponing their first payment, even if it means higher upfront interest. Conversely, those seeking immediate budget relief might opt for early closings with lender credits:

- FHA/VA loans: Interest credits often available for closings by the 7th

- Conventional loans: Credits typically apply to closings by the 10th

Tax and Insurance Considerations

Closing dates also influence property tax and insurance prepayments:

- Taxes: Buyers typically prepay 14 months of property taxes at closing

- Insurance: Two months of hazard insurance premiums are usually required

For refinances, closing dates affect interest proration between old and new loans but don’t change total costs. A January 8 refinance would split interest between the old loan (8 days) and new loan (23 days), while a January 28 closing would reverse this split.

Key Takeaways

- Late-month closings reduce upfront interest but accelerate first payments

- Mid-month settlements may improve service quality and accuracy

- Lender credits can offset early-closing costs for qualifying borrowers

- Always weigh cash flow needs against long-term payment schedules