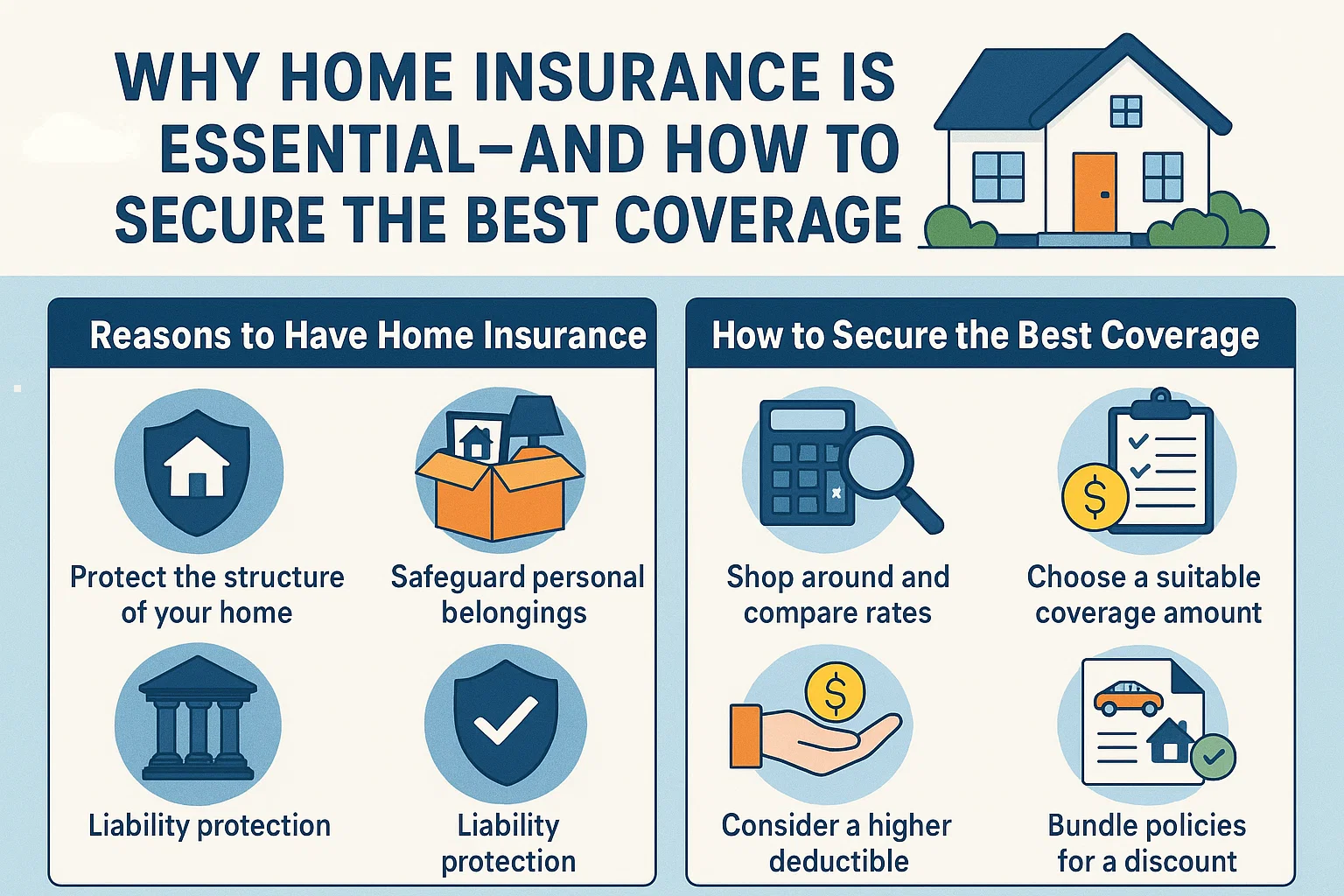

Why Home Insurance Is Essential—and How to Secure the Best Coverage

Buying Insurance for Your New Home Isn’t a Matter of Maybe. It’s a Must.

Your mortgage lender requires it. And as a matter of financial common sense, you should have it for your own protection and peace of mind. Here are some pointers on getting the best deal.

What’s Not Covered

Homeowners insurance is not just about what’s covered, but what’s NOT. Most standard policies cover your risk of loss from major hazards:

- Fires

- Lightning strikes

- Roof damage

- Ice and snow

- Plumbing system breakdowns

- Explosions

But ask about language buried in the block print of the insurance contract that may limit coverage for situations like wind damage and long-term pipe leakages. If you’re in an area with exposure to hurricanes, violent thunderstorms, or tornados, standard policies may only cover a small portion of repair expenses. Extended coverage may be necessary.

Comparison Shop

Compare home insurance like you comparison-shopped for a mortgage:

- Start with your current auto insurer—discounts often apply for bundling policies.

- Consult a local independent agent who works with multiple insurers.

- Get quotes from companies that sell directly to consumers.

- Ask your builder, lawyer, or realty agent for recommendations.

Understanding Homeowners Insurance

Key components include:

- Deductibles: The amount you pay before insurance kicks in. Higher deductibles mean lower premiums.

- Premiums: Monthly or annual payments for coverage.

- Exclusions: Damages the insurer won’t cover (e.g., floods, earthquakes).

Homes in flood zones require separate coverage via the National Flood Insurance Program.

Protect Personal Items

- Standard policies cover personal property up to a percentage of your home’s value (e.g., 75%).

- Check limits for valuables like jewelry, antiques, or art. Purchase additional coverage if needed.

- Document possessions with photos or video for claims.

- Opt for replacement cost over actual cash value to avoid depreciation deductions.

- Consider loss of use coverage for temporary lodging after severe damage.

Extended Replacement Costs

Choose Extended Replacement Cost coverage with an inflation guarantee. This ensures:

- Rebuilding costs up to a percentage above your insured amount.

- Adjustments for rising market values in fast-appreciating areas.

Final Tips

Home insurance requires anticipating gaps in coverage. Research regional weather risks, document belongings, and review policies annually. With careful planning, you can safeguard one of your most valuable assets: your home.