Know How Your Credit Score Gets Calculated, So You Can Get It Ready to Apply for a Mortgage

Know How Your Credit Score Gets Calculated, So You Can Get It Ready to Apply for a Mortgage

Before you apply for a mortgage, it’s important to know what’s in your credit report. Here’s how to check it for free.

Why Your Credit Report Matters

If you’re thinking about buying a new home, checking your credit report is essential. While credit reports from the three national credit bureaus (Equifax, TransUnion, and Experian) are generally accurate, even a small error could affect your ability to secure the best mortgage rate—or qualify for a loan at all.

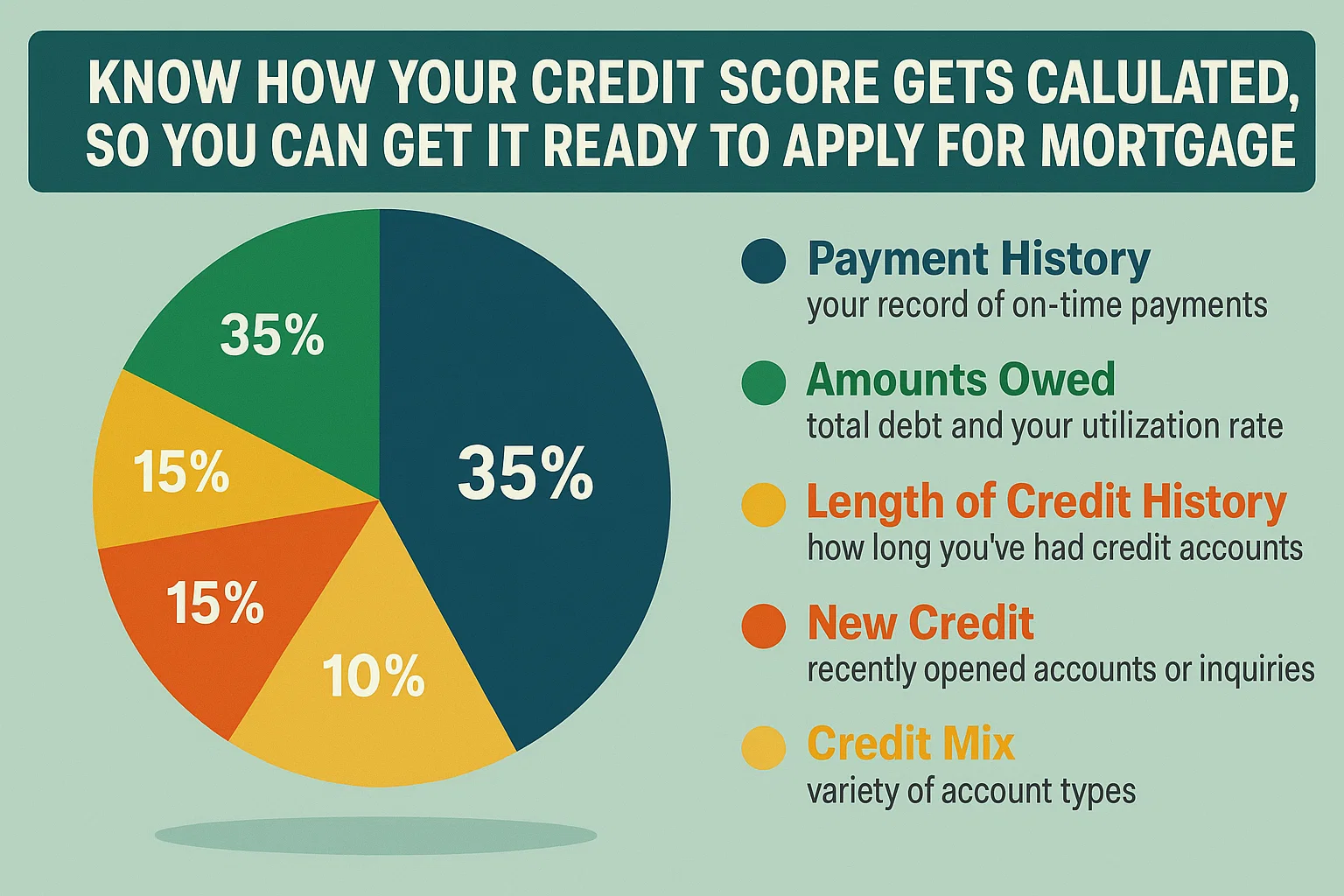

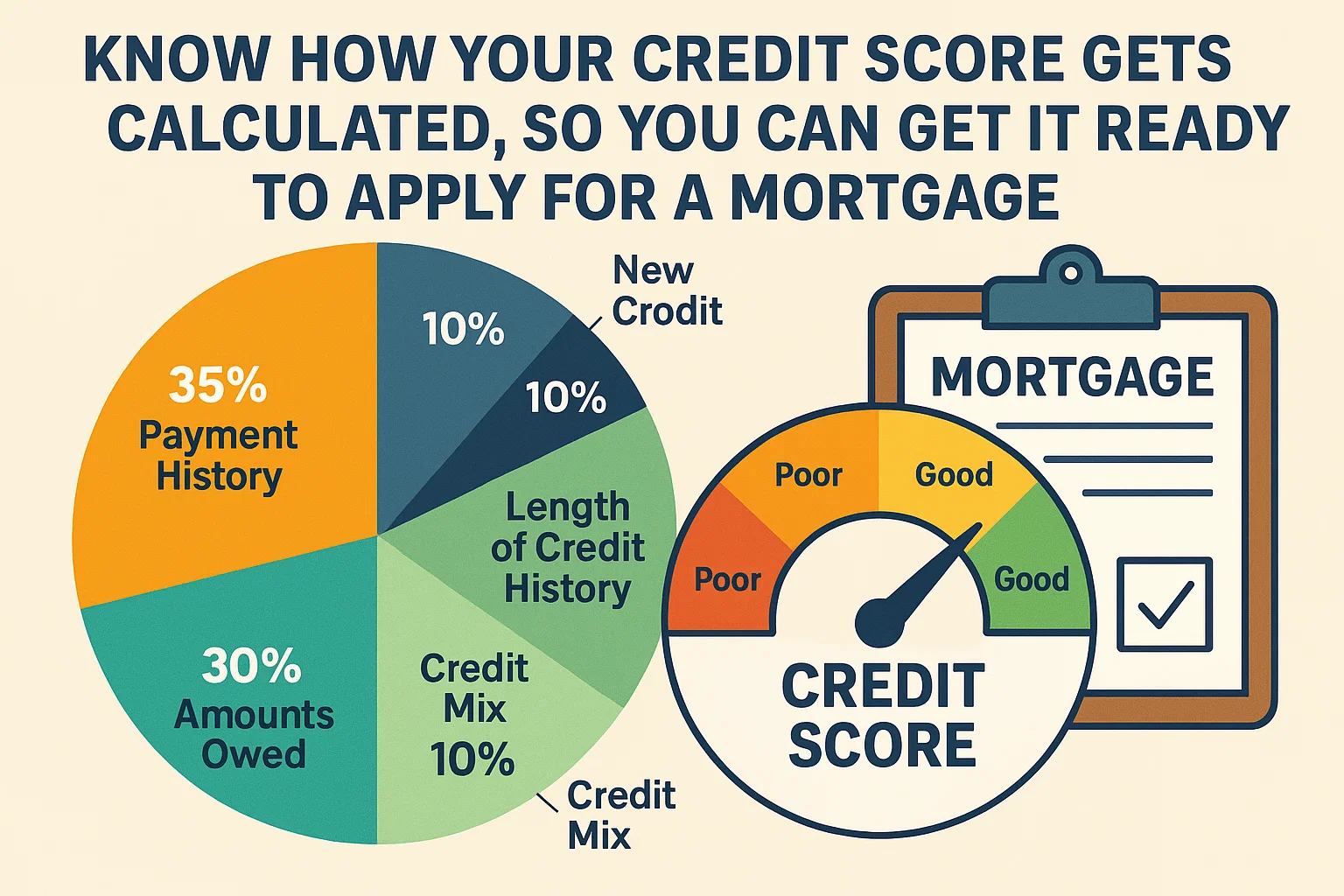

Credit reports are a cornerstone of lending decisions. They include your borrowing history, addresses, lawsuits, arrests, and bankruptcies. Lenders also consider factors like income and employment history, but your credit behavior is a critical predictor of whether you’ll make timely mortgage payments.

The Risk of Errors

A Federal Trade Commission (FTC) study found:

- 1 in 4 consumers found errors in their credit reports.

- 1 in 20 discovered mistakes that could lower their credit scores by at least 25 points.

- 1 in 250 identified inaccuracies that reduced scores by 100 points or more.

While these percentages may seem low, errors can take weeks to resolve—if they’re fixed at all. To avoid delays, review your credit report at least three months before applying for a mortgage.

How to Access Your Free Credit Reports

By law, you’re entitled to one free credit report annually from each of the three major bureaus. Visit AnnualCreditReport.com to request yours. Avoid other sites offering “free” reports, as they often upsell paid services. The reports from AnnualCreditReport.com are identical to those lenders use.

Request reports from all three bureaus, since lenders may pull different ones, and creditors don’t always report to all three. For example, your auto loan might appear on only one report, while a retail account could show up on another.

Reviewing Your Reports

Look for:

- Accounts you don’t recognize.

- Incorrect payment history or credit limits.

- Outdated negative information (e.g., bankruptcies or late payments past the reporting period).

Disputing Errors

Under the Fair Credit Reporting Act (FCRA), credit bureaus and data providers must investigate disputes. To start the process:

- File a dispute online, by mail, or by phone with the relevant bureau.

- Keep copies of all correspondence, including names, dates, and case numbers.

- Be concise and polite—avoid emotional appeals.

Bureaus have 45 days to respond. If an error is confirmed, the provider must notify all three bureaus to update your file. If you disagree with the outcome, you can add a 100-word statement to your report explaining your perspective.

Timing of Negative Information

Accurate negative items generally remain on your report for:

- 7 years: Foreclosures, late payments, unpaid judgments.

- 10 years: Bankruptcies.

Beware of credit repair companies promising quick fixes. They often charge upfront fees (illegal under the Credit Repair Organizations Act) and temporarily hide negative items—only for them to reappear later.

Take Control of Your Credit

Understanding your credit report puts you in a stronger position to buy a home. Address errors early, monitor your history, and avoid costly scams. With preparation, you’ll be ready to secure the mortgage you need.