As a Prospective Homebuyer, Should You Build a New Construction Home?

As a Prospective Homebuyer, Should You Build a New Construction Home?

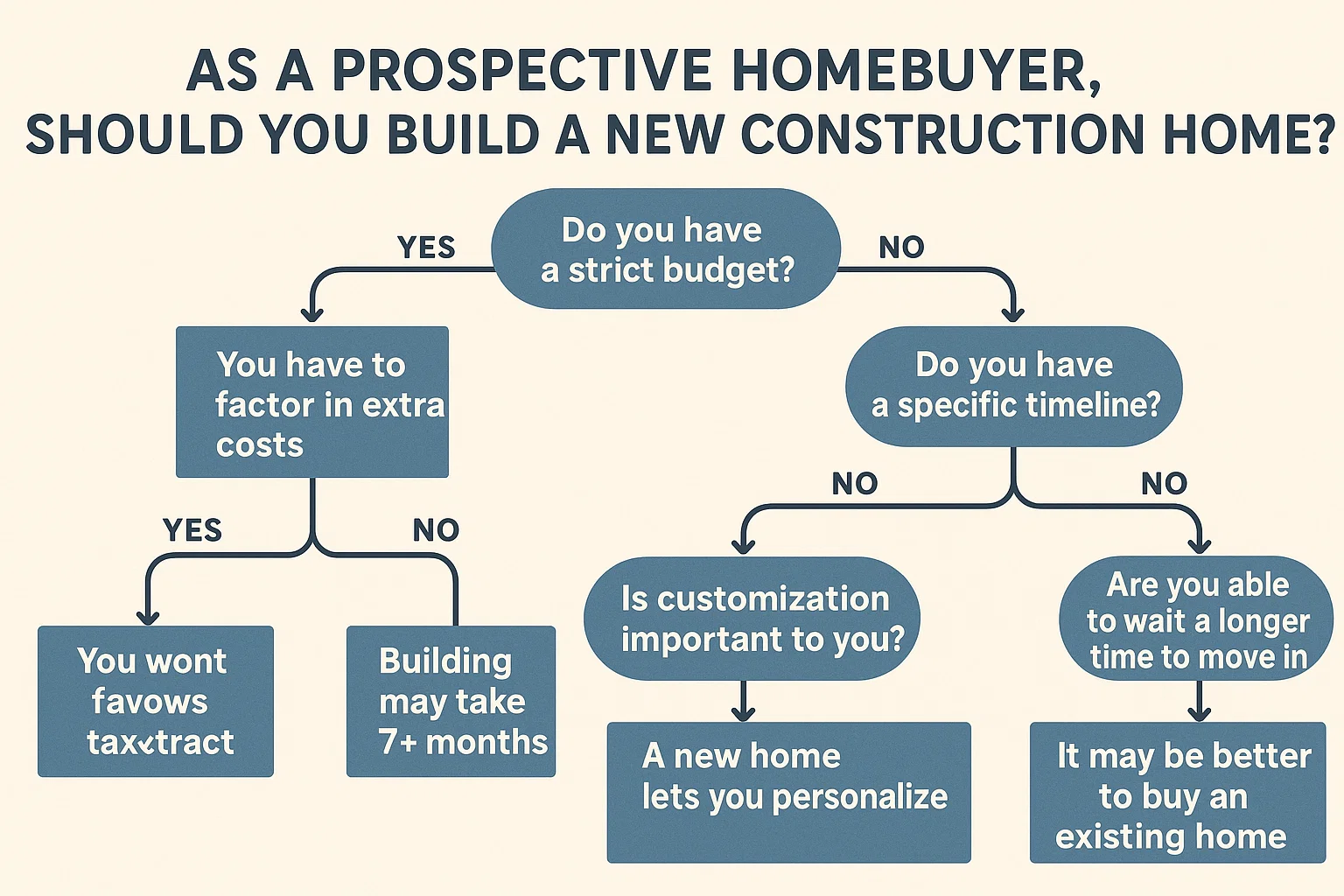

As a prospective homebuyer, you might be considering building a new home instead of purchasing an existing one. If you decide to build a new construction home, it is critical to research and secure a construction loan that aligns with your financial situation. Below, explore the most common types of new construction loans and determine which option suits your project best.

Construction-to-Permanent Loan

A construction-to-permanent loan, also known as a single-close loan, combines financing for land purchase, construction, and the final mortgage into one package. This eliminates the need for separate loans for each phase of the project.

Benefits

- Single closing process reduces overall fees.

- Funds are drawn incrementally during construction, with interest paid only on the amount used.

- Up to 18 months of flexibility for construction delays.

- Automatically converts to a fixed-rate mortgage (15–30 years) upon completion.

Drawbacks

- Limited lender availability and stringent approval requirements.

- High fixed interest rates during construction, which may not decrease afterward.

- Interest-only payments for up to 18 months before principal payments begin.

- Typically requires a 20% down payment and detailed construction documentation.

Construction-Only Loan

A construction-only loan covers land purchase and building costs but must be repaid or refinanced into a mortgage once construction ends.

Benefits

- Ideal for those planning to sell their current home to fund the new build.

- Separates construction financing from the permanent mortgage.

Drawbacks

- Requires two separate closings, increasing fees and paperwork.

- Borrowers must qualify for a new mortgage after construction.

Owner-Builder Construction Loan

This loan is designed for individuals acting as their own general contractor during construction.

Benefits

- Greater control over budget and construction decisions.

Drawbacks

- Limited availability and rigorous approval process.

- Requires proven experience in home building or contracting.

Hard Money Construction Loan

A short-term, high-interest loan often used for investment properties or urgent projects.

Benefits

- Fast approval based on property value, not credit history.

- Flexible terms from private lenders or investors.

Drawbacks

- High interest rates and large down payments.

- Short repayment periods and higher risk of property seizure.

Choose the Loan That Works for You

Building a new home offers customization and long-term value, but selecting the right loan requires careful consideration. Research all options, consult financial professionals, and evaluate your financial readiness. By doing so, you can ensure your new construction home becomes a rewarding investment tailored to your lifestyle.