Common Mistakes First-Time Homebuyers Must Avoid

Common Mistakes First-Time Homebuyers Must Avoid

Don’t Apply for Another Loan

One loan officer shared an example of a couple who jeopardized their home purchase by financing a luxury car before closing. The new monthly payment pushed their debt-to-income ratio above the recommended 43%, ultimately derailing the sale. Experts warn against opening new lines of credit—even for furniture, appliances, or store credit cards—until after closing. A seemingly small $500 credit limit could tip the scales unfavorably.

“You may need that new washer and dryer, but they can knock you completely out of a loan if it’s a tight squeeze with your income.”

Don’t Make a Big Job Change

Switching jobs during the loan process isn’t automatically disqualifying, but abrupt career shifts or changes in pay structure (e.g., moving to commission-based work) can raise concerns. A senior loan officer explained, “If you’re doing something brand new, it could signal shaky stability to underwriters.” Always inform your lender about employment changes to avoid delays.

Don’t Have Unexplained Fluctuations on Your Bank Statements

Large deposits or withdrawals must be documented. A lending executive emphasized, “We need to source all of your down payment to ensure it’s your money.” Gifts, crowdfunding, or asset sales require proof, while unexplained transactions may prompt additional scrutiny or loan denial.

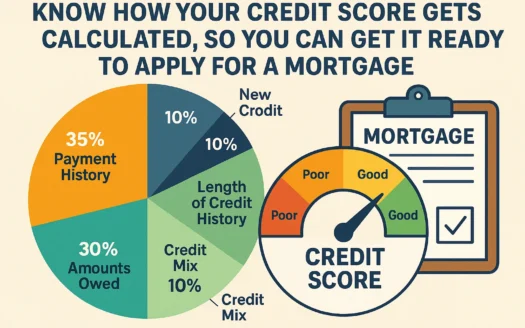

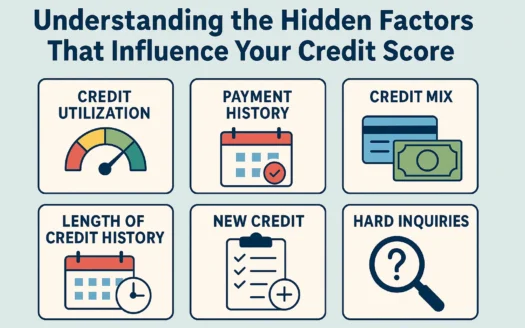

Don’t Close Out Lines of Credit

Paying down debt is wise, but closing accounts can erase valuable credit history. Experts recommend keeping cards open and maintaining balances below 30% of the limit. “Buy $30 worth of gas to keep the account active, but don’t close it until after you’re in the home,” advised one professional.

Don’t Try to Hide Financial Bruises

Lenders will uncover debts during underwriting. Transparency helps loan officers structure viable solutions. “We’re there to help you close the loan, not spend months on an application that fails,” noted an expert. Disclosing issues early allows for strategies like paying off small debts quickly.

Don’t Go In Unprepared

Many first-time buyers need credit cleanup or longer employment history to secure affordable loans. Experts stress working with financial counselors to build savings habits and consistent payment patterns. “Six months of job history is a start, but we need to see long-term behavior,” one lender cautioned.

from Unsplash