A Comprehensive Guide to FHA Loans: Benefits, Types, and Eligibility

A Comprehensive Guide to FHA Loans: Benefits, Types, and Eligibility

What Is an FHA Loan?

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration (FHA). This insurance reduces risk for lenders, allowing them to offer loans to borrowers who might not qualify for conventional financing. If a borrower defaults, the FHA compensates the lender, making these loans more accessible for individuals with limited savings or credit challenges.

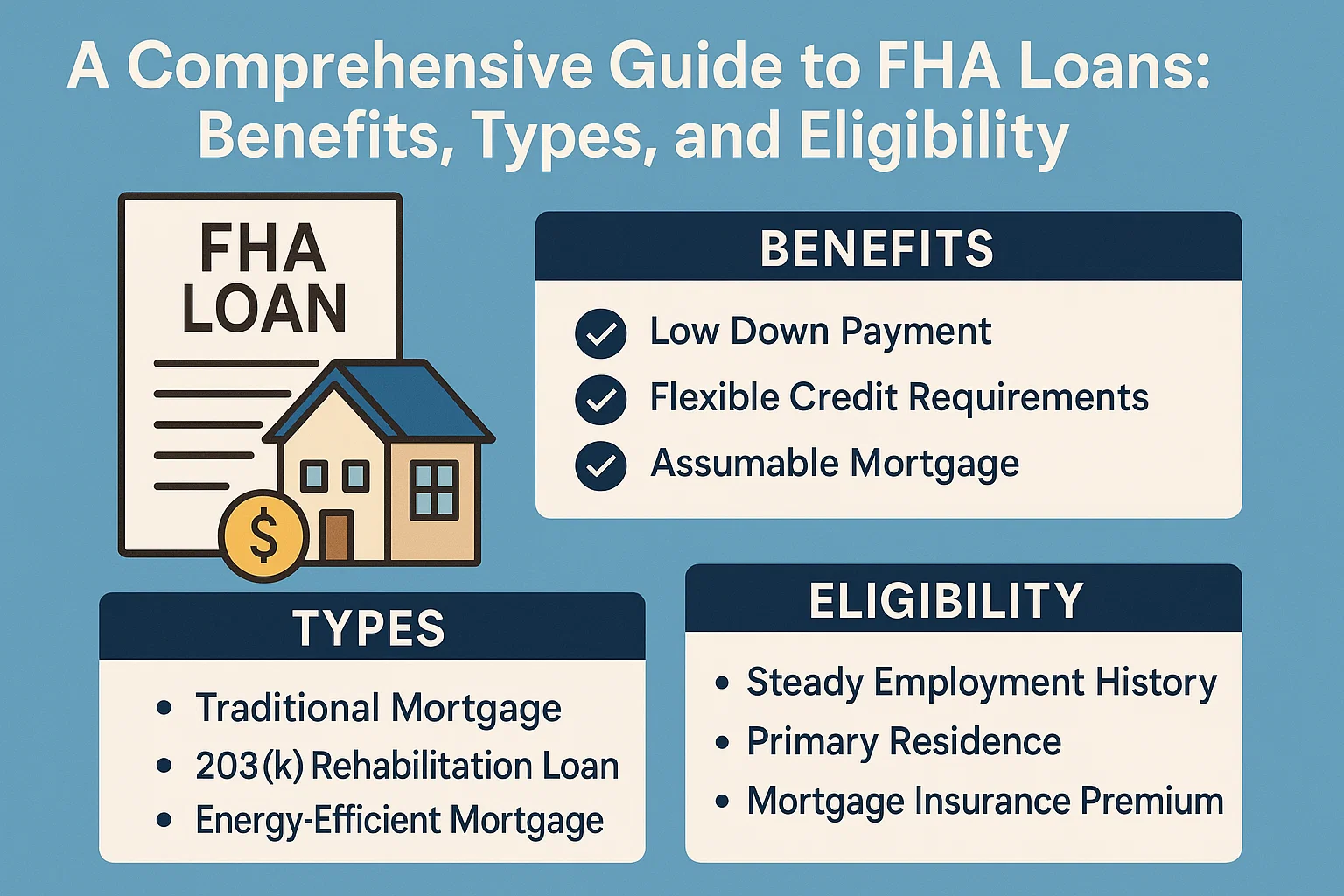

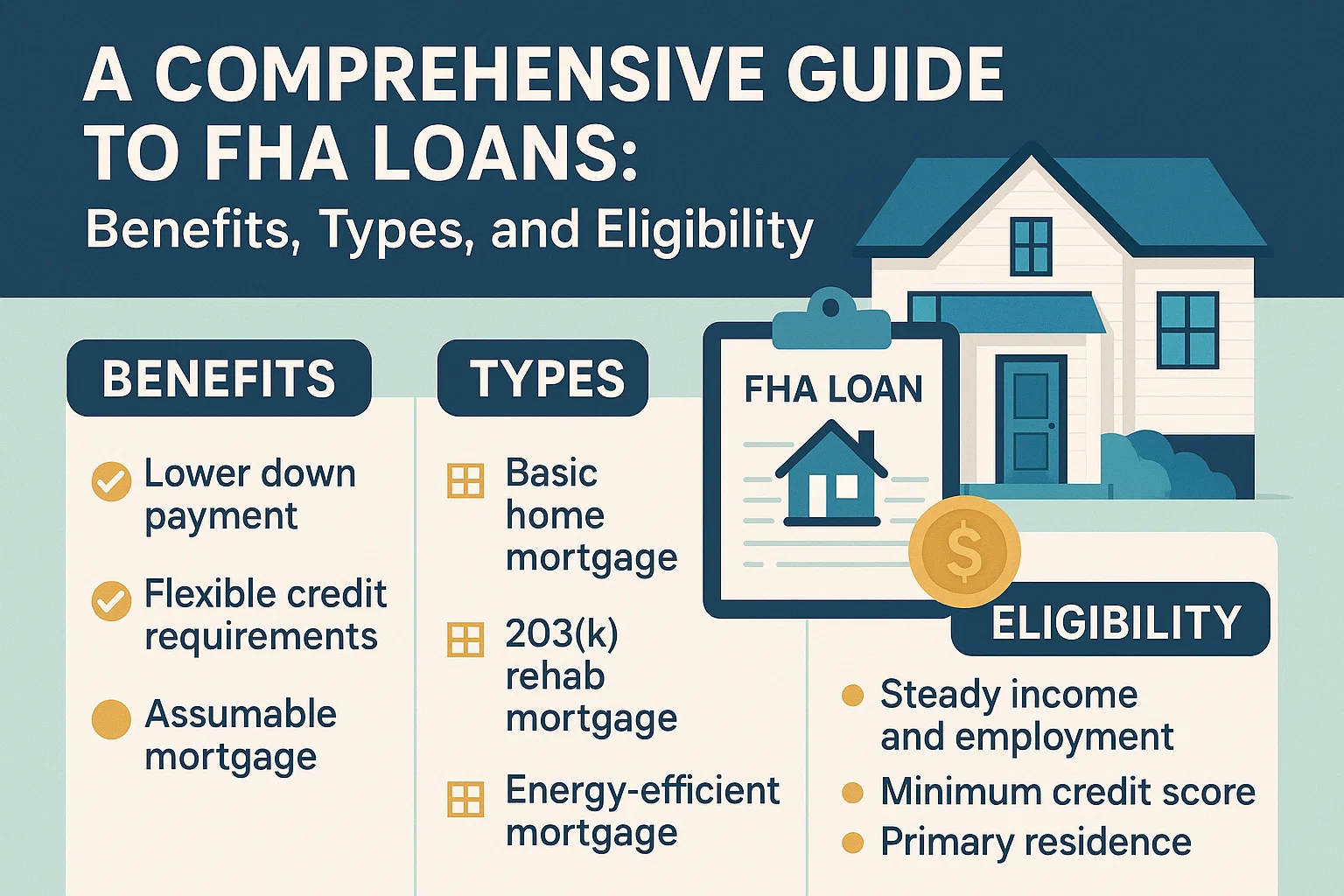

Key Benefits of FHA Loans

- Lower Credit Requirements: Minimum credit score of 580 (vs. 620+ for conventional loans).

- Small Down Payment: As low as 3.5% down payment required.

- Flexible Debt-to-Income Ratio: Allows higher debt levels relative to income.

- Affordable Mortgage Insurance: Lower premiums compared to conventional loans with less than 20% down.

Types of FHA Loans

- Basic Home Mortgage (203(b)): Standard loan for purchasing or refinancing a primary residence.

- Rehabilitation Mortgage (203(k)): Funds home repairs and renovations.

- Energy Efficient Mortgage (EEM): Supports energy-saving upgrades for new or existing homes.

- Home Equity Conversion Mortgage (HECM): Reverse mortgage option for seniors aged 62+.

Eligibility Requirements

- Credit Score: Minimum 580 for 3.5% down payment (500-579 with 10% down).

- Debt-to-Income Ratio: Typically below 43%.

- Primary Residence: Must be used for a primary home, not rental or investment properties.

- Property Standards: Home must meet FHA safety and livability guidelines.

Who Should Consider an FHA Loan?

- First-Time Homebuyers: Low down payment and credit flexibility ease entry into homeownership.

- Borrowers with Limited Savings: Ideal for those unable to afford a 20% down payment.

- Credit-Challenged Applicants: More forgiving of past financial setbacks.

- Homeowners Seeking Renovations: Use a 203(k) loan to finance repairs during purchase.

When to Explore Alternatives

- High-Cost Areas: FHA loan limits may restrict borrowing power in expensive markets.

- Rental or Investment Properties: FHA loans are exclusive to primary residences.

- Significant Home Repairs Needed: Properties must meet minimum safety standards at purchase.

- Strong Credit and Savings: Conventional loans may offer better terms for qualified buyers.

Final Considerations

FHA loans provide a valuable pathway to homeownership for many borrowers, but they aren’t universally ideal. Assess your financial situation, long-term goals, and property needs to determine if an FHA loan aligns with your priorities. Always compare multiple mortgage options to secure the best terms for your circumstances.