Your Guide to Securing a Mortgage for a New Construction Home

Your Guide to Securing a Mortgage for a New Construction Home

Understanding Your Loan Options

Building or buying a new home involves two primary financing paths:

Construction Loans

Purpose: Funds the building of a property from the ground up, including materials and labor. Often paired with lot financing loans. These are short-term loans that typically convert into long-term mortgages (15 or 30 years) after construction completes.

New Construction Home Loans

Purpose: Used to purchase a newly built home from a developer or builder. Builders in established developments may offer affiliated lenders to streamline the process, creating a seamless experience similar to buying an existing home.

Preparing for Your Mortgage Journey

Step 1: Assess Your Loan Needs

- Custom builds require construction loans.

- Developments with turnkey services may offer builder-affiliated lenders for simplified financing.

Step 2: Consult a Lender

Meet with a lender early to:

- Review loan products and eligibility requirements

- Clarify budget expectations

- Address credit readiness

Step 3: Strengthen Your Credit

- Obtain free credit reports from Experian, Equifax, and TransUnion.

- Dispute errors and address late payments.

- Ask lenders about credit repair assistance programs.

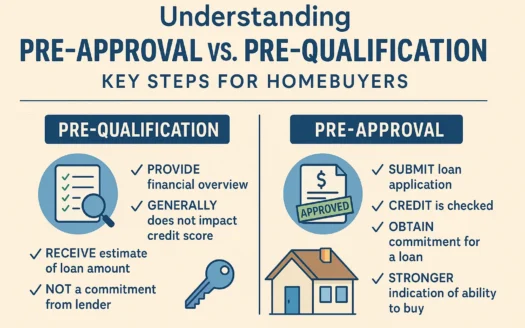

Step 4: Secure Pre-Approval

Gather documentation to verify:

- Income (pay stubs, tax returns)

- Assets (bank statements)

- Debt obligations

A pre-approval letter clarifies your purchasing power and strengthens your position when finalizing home plans.

Final Thoughts

By understanding loan types, improving credit health, and securing pre-approval, you can confidently navigate the financing process for your new home. Partner with lenders early to align your budget with your vision and create a stress-free path to homeownership.