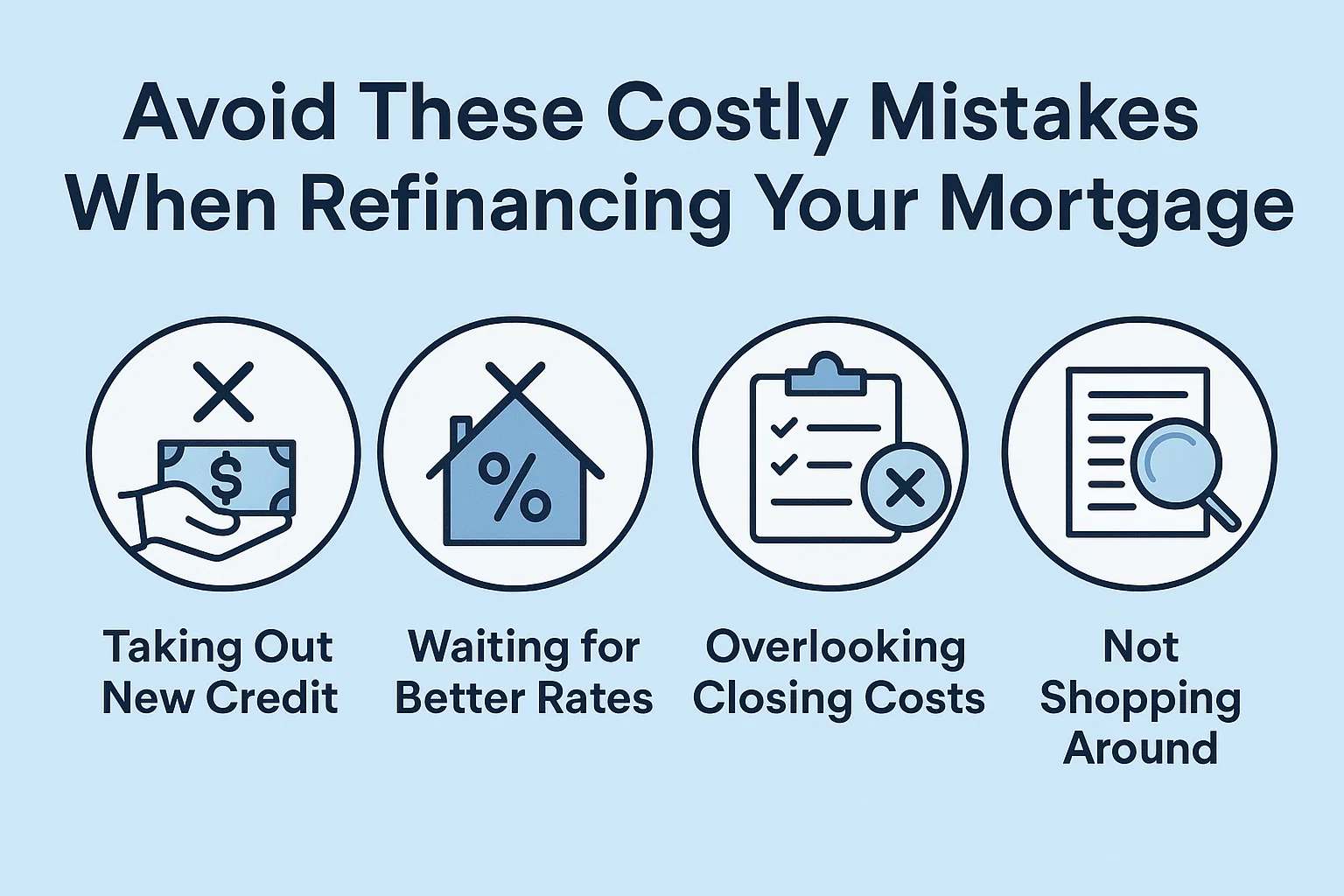

Avoid These Costly Mistakes When Refinancing Your Mortgage

Avoid These Costly Mistakes When Refinancing Your Mortgage

With mortgage rates hovering near historic lows, many homeowners feel pressured to refinance quickly. While the potential savings are enticing, rushing into a refinance without careful planning can lead to costly errors. Below are three critical mistakes to avoid during the refinancing process.

Mistake #1: Underestimating Your Home’s Value

Why it matters: Your home’s equity directly affects your refinancing terms. A higher valuation can lower your interest rate and eliminate the need for private mortgage insurance (PMI), which is typically required if you have less than 20% equity.

Solution: Obtain a comparative market analysis from a local real estate agent or a broker’s price opinion. For a more precise figure, consider a professional appraisal (costing a few hundred dollars).

Mistake #2: Neglecting Your Credit Score

Why it matters: Your credit score determines the interest rate lenders offer. A higher score can save thousands over your loan’s lifespan.

How to optimize your score:

- Fix errors: Dispute inaccuracies on your credit report and address late payments or unpaid bills.

- Manage debt responsibly: Avoid opening multiple credit accounts, carrying high balances, or exceeding credit limits.

- Build positive habits: If possible, wait 6 months to demonstrate consistent on-time payments and reduced debt.

Mistake #3: Failing to Negotiate Closing Costs

Why it matters: Refinancing fees—including lender charges, title fees, and escrow—can add thousands to your costs. These are often rolled into your monthly payment, making them easy to overlook.

Solution:

- Compare offers: Shop around and use competing quotes to negotiate better terms.

- Leverage your credit score: A strong credit profile gives you more bargaining power.

Final Tips for a Smooth Refinance

While refinancing can lower your monthly payments, thorough preparation is key to avoiding expensive missteps. Always research your home’s value, prioritize credit health, and negotiate fees aggressively. Consulting a mortgage professional can also help you secure the best possible terms.